Every Document California Home Buyers Must Sign — From Search to Close

California buyer disclosures don’t start when the seller hands you a packet. They start before you tour your first home – and they run all the way to the day you sign loan documents at closing.

The TDS, NHD, and AVID that arrive after you go under contract. They’re useful, but they don’t tell the whole story.

Most buyers find this out the hard way. They receive a 60-page disclosure packet, sign an acknowledgment, and move on. What they miss are the cancellation windows, the red flags embedded in legal language, and the rights that expire quietly if nobody tells them to act.

This guide covers every document across all four stages of a California home purchase: what each one is, what to check, and what rights it creates or takes away.

If you are buying a home in California in 2026, this guide to California buyer disclosures gives you the complete picture.

Updated for 2025–2026.

This guide reflects AB 2992 (mandatory BRBC before first MLS tour, effective January 1, 2025), C.A.R. Form SPQ Rev. Dec 2024 (new electrical and gas appliance disclosures), and the FinCEN beneficial ownership requirement added to the RPA (effective March 1, 2026).

California Buyer Disclosures: The Complete 4-Stage Timeline

Use this table as your master reference throughout the transaction. Every legally significant document, who provides it, when it arrives, and what you can do with it.

| Document | Required? | Law / Form | What it covers | What buyers should check |

|---|---|---|---|---|

| Pre-search / pre-offer | ||||

| Buyer-Broker Representation Agreement (BRBC) | Yes (to tour MLS) | AB 2992; C.A.R. BRBC Rev. 12/24 | Agency relationship, agent compensation, exclusivity, 90-day max term. Required before first MLS tour. | Exclusivity (default: non-exclusive). Compensation if seller doesn’t pay. Property/geography scope. End date. |

| Agency Relationship Disclosure (AD) | Yes | CC §2079.14 | Discloses who your agent represents: you only, seller only, or both (dual agency). | Dual agency limits agent advocacy for you. Know before signing. |

| Mortgage application | ||||

| Loan Estimate (LE) | Yes | TRID / Reg Z §1026.19(e) | Standardized 3-page federal form: rate, monthly payment, closing costs, APR. From lender within 3 business days of application. | Compare Section A across 3+ lenders. Check APR vs. rate gap. Rate lock status. |

| Intent to Proceed | Yes | TRID / CFPB | You authorize lender to proceed. No fees can be charged before this, except a credit report. | Don’t sign until satisfied with the Loan Estimate. No obligation to use that lender after signing. |

| Under contract (within 17 days) | ||||

| Residential Purchase Agreement (RPA) | Yes | C.A.R. Form RPA | The binding contract: price, contingency periods, deposits, closing date, disclosure delivery timelines. | All contingency period lengths. Deposit at risk after contingency removal. Disclosure delivery deadline (7 days). |

| Transfer Disclosure Statement (TDS) | Yes | CC §1102 | Seller’s known material defects: roof, plumbing, electrical, structural, pest, HOA, legal claims, deaths within 3 years. | Every “Yes” answer. Repaired issues. Prior inspection reports. Blank fields. |

| Seller Property Questionnaire (SPQ) | Yes | C.A.R. Form SPQ Rev. 12/24 | Supplements TDS: prior reports/permits, fill/grading, drug lab, insurance claims, 2025 gas/electrical disclosures. | All prior inspection reports. Unpermitted work. Insurance claims. |

| Natural Hazard Disclosure (NHD) | Yes | CC §1103 | 6 mandatory zones: flood, dam, Very High Fire (HFHSZ), wildland fire, earthquake fault, seismic hazard. | HFHSZ means verify insurance before removing contingencies. Any “Yes” can mean added cost or risk. |

| Agent Visual Inspection Disclosure (AVID) | Yes | CC §2079 | Listing agent’s independent visual observations. Must be completed before contingency removal. | Divergence from TDS is a red flag. Late delivery is a compliance issue. |

| Lead-Based Paint Disclosure (pre-1978) | Yes (pre-1978) | 42 USC §4852d | Known lead paint, EPA booklet, 10-day testing window (waivable). | Don’t waive testing if you plan renovations. |

| Water Heater Seismic Strap Certification | Yes | CA H&S §19211 | Seller certifies the water heater is strapped per California law. | Verify physically during inspection. It is a code issue if missing. |

| Smoke / CO Detector Compliance | Yes | CA H&S §13113.8 | Operable smoke detectors at time of sale; CO detectors for homes with garages or fossil fuel appliances. | Verify certifications are signed. It is a small fix, but it still must be completed before close. |

| HOA Documents (condos / planned developments) | If HOA | CC §4525 | CC&Rs, bylaws, budget, reserve study, special assessments, meeting minutes, pending litigation, master insurance. | Reserve fund below 70% can signal special assessment risk. Check pending litigation. |

| Supplemental / Amended Disclosure | If new info arises | CC §1102.3(c) | If the seller learns new material information after TDS delivery, they must amend. Revives cancellation rights. | Even after contingency removal, the 3-day personal / 5-day electronic cancellation right may be revived. |

| Closing | ||||

| Closing Disclosure (CD) | Yes | TRID / Reg Z §1026.19(f) | Final loan terms, actual closing costs, and cash to close. Must arrive 3 business days before signing. | Compare line by line to the Loan Estimate. Flag any fee increases over tolerance. |

| Promissory Note + Deed of Trust | Yes | State + Federal | Your legal promise to repay the loan and the lender’s lien on the property. | Confirm rate, loan amount, and prepayment terms match the Closing Disclosure before signing. |

Stage 1: Before Your First Tour – BRBC and Agency Disclosure

What Are California Buyer Disclosures at the Pre-Offer Stage?

Most buyers think disclosures begin after they go under contract. In California, they begin before you walk through a front door.

Two documents define your legal relationship with your agent before you ever make an offer. Understanding both of them protects you at every stage that follows. These California buyer disclosures are your legal record of what was disclosed, when, and by whom.

Buyer-Broker Representation Agreement (BRBC)

The BRBC is the most consequential change to California real estate since 2025. Under Assembly Bill 2992, which took effect January 1, 2025, every buyer’s agent must have a signed written agreement in place no later than the moment a buyer submits an offer. In practice, the NAR settlement (August 2024) pushed this earlier – agents now present the BRBC before any MLS-listed showing.

So the reality is simple: you will sign this contract before you tour your first listed home with an agent.

The BRBC is a legally binding contract, not a formality. Under AB 2992 and CC §1670.50, the term cannot exceed 90 days. Any agreement written for longer than 90 days is void and unenforceable from inception. Read it before you sign it.

| BRBC Term | What it means for you | What to check / negotiate |

|---|---|---|

| Representation period | Maximum 90 days by law (AB 2992, CC §1670.50). If it exceeds 90 days, the agreement is void and unenforceable. | Make sure the end date is clearly written. Avoid open-ended agreements. |

| Exclusive vs. non-exclusive | Default is non-exclusive — agent gets paid only if involved in your purchase. Exclusive means agent gets paid even if you find the home yourself. | Non-exclusive protects you more. If exclusive is checked, understand what “involved” means. |

| Agent compensation amount | Must be a specific dollar amount or percentage — not vague. You are responsible if the seller doesn’t offer to cover it. | Ask: “What happens if the seller doesn’t pay your commission?” Understand your exposure before signing. |

| Property type / geography | Defines what properties the agreement covers (single-family, condos, certain cities, price range). | Make sure it matches what you’re actually searching for. Don’t sign a BRBC covering all of California if you’re only looking in one city. |

| Cancellation rights | Non-exclusive: either party can cancel. Exclusive: unilateral cancellation effective 30 days after written notice to the other party. | If exclusive, factor the 30-day notice period into your timeline. |

What happens if the seller doesn’t offer to pay your agent’s commission?

Under the post-NAR settlement framework, sellers are no longer required to offer buyer agent compensation through the MLS.

If the seller doesn’t offer to pay, the BRBC holds you responsible. Most agents negotiate this as part of the offer by asking the seller to cover the buyer’s agent fee as a seller concession.

However, this is being negotiated deal-by-deal as of today, doesn’t happen automatically. [A]

This is relevant to your budget planning: factor in the possibility that you’ll need to cover agent compensation as part of your closing cost budget if the seller won’t.

Agency Relationship Disclosure (C.A.R. Form AD)

Before any offer, your agent is required to provide this form confirming who they represent. The distinction matters more than most buyers realize.

- Single agency: Your agent represents you exclusively. They owe you full fiduciary duties: loyalty, confidentiality, and disclosure.

- Dual agency: The same agent or brokerage represents both buyer and seller. They cannot fully advocate for either party, and that limitation has real consequences in a negotiation.

Dual agency requires your written consent.

If you are a first-time buyer, insist on single agency. The agent showing you a property may well be the listing agent. Know what they can and cannot do for you in that situation before you rely on their guidance.

Stage 2: Mortgage Application – Loan Estimate and Intent to Proceed

Loan Estimate

The Loan Estimate is a standardized 3-page federal form required under the TILA-RESPA Integrated Disclosure (TRID) rule. Your lender must deliver it within 3 business days of receiving a complete loan application.

A complete application means you have submitted your name, income, Social Security number, property address, estimated property value, and the loan amount you are requesting. Until all six pieces of information are in, the lender has no obligation to issue a Loan Estimate, regardless of what preliminary conversations you have had.

The Loan Estimate replaced the old Good Faith Estimate in 2015. It is your single best tool for comparing lenders. Most buyers get one and stop. That is a costly mistake.

The most important action you can take at this stage: get Loan Estimates from at least three lenders on the same day.

Origination fees alone vary by $2,000 to $5,000 between lenders on the same loan amount. Because mortgage applications within a short window count as a single credit inquiry, applying to multiple lenders carries minimal credit score impact. The comparison costs you nothing but time.

| Loan Estimate section | What it shows | What to compare across lenders | Red flag |

|---|---|---|---|

| Page 1 — Loan Terms | Loan amount, interest rate, monthly P&I, prepayment penalty, balloon payment | Rate and P&I payment | Rate lock not checked; balloon payment present |

| Page 1 — Projected Payments | Monthly payment breakdown including taxes, insurance, MIP/PMI | Total monthly cost (PITI) | PMI/MIP not disclosed when <20% down |

| Page 1 — Costs at Closing | Total closing costs + cash to close (including down payment) | Total closing costs estimate | Large “other” or unexplained line items |

| Page 2 — Section A: Origination | Lender fees: origination, underwriting, processing, points | This is where lenders vary most — compare Section A directly | Origination >1% without rate reduction; undisclosed points |

| Page 2 — Section B/C: Services | Appraisal, title, escrow — some you can shop, some you can’t | Section C “services you can shop” — get your own quotes | High title or escrow fees vs. other lender estimates |

| Page 3 — Comparisons | APR, Total Interest Percentage (TIP), and in 5 years totals | APR (most inclusive rate measure) and TIP | Large gap between rate and APR = high fees |

Important: Once you sign the Intent to Proceed (the form authorizing the lender to continue), you have limited ability to switch lenders easily. Get your comparisons done before you sign. The lender also cannot charge most fees before you sign the Intent to Proceed — except a reasonable fee for your credit report. [B]

Intent to Proceed

After reviewing your Loan Estimate, you sign a short form authorizing the lender to move forward with your application. Signing this does not obligate you to close with that lender, but it does start the clock on several commitments.

Before you sign, do the following:

- Compare at least two or three Loan Estimates.

- Once you sign the Intent to Proceed, your appraisal will be ordered – and that cost, typically $500 to $1,000, is non-refundable.

- Your rate lock period also begins around this time, so understand the lock terms before you commit.

Lenders cannot charge most fees before you sign the Intent to Proceed. The only exception is a reasonable fee for pulling your credit report.

Stage 3: Under Contract – Reviewing California Buyer Disclosures in the 17-Day Window

Your Disclosure Timeline Under the RPA

Once your offer is accepted on Day 0, the California Residential Purchase Agreement sets the clock running. The seller typically has 7 days to deliver all required disclosures. You have 17 days for inspections and review, though that period is negotiable in your contract.

| Timing | Document(s) | Your right | Law |

|---|---|---|---|

| Day 0 | Offer accepted (RPA signed) | 17-day contingency period begins (default) | C.A.R. RPA §L3 [C] |

| Within 7 days | TDS, SPQ, NHD, AVID, Lead Paint, Megan’s Law, Agency Disclosure | 3 days (personal) or 5 days (email/mail) to cancel after receipt | CC §1102.3; RPA §N1 [C] |

| ASAP (varies) | HOA documents (if condo/planned development) | Separate contingency. Write your HOA review period into the contract. | CC §4525 [C] |

| Within 17 days | Buyer-ordered inspection reports | Request credits or cancel before contingency deadline | RPA §L3 [C] |

| Any time before close | Supplemental / amended disclosures (if new info arises) | 3 days (personal) / 5 days (electronic) to cancel, even if contingencies are already removed | CC §1102.3(c) [C] |

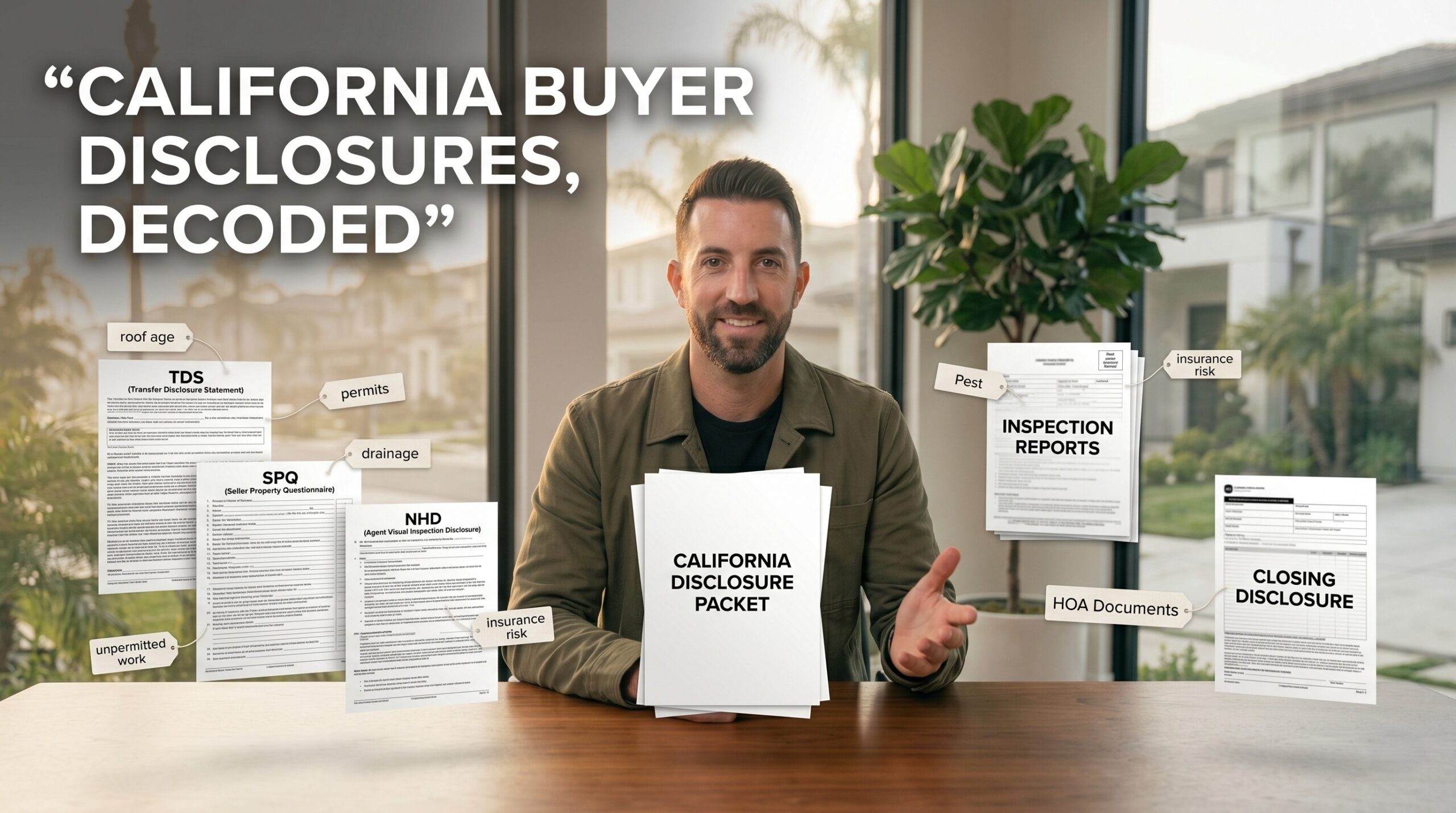

The Core Seller Disclosures

The following five documents form the seller disclosure package in every California home sale. Each one has specific things to check and specific cancellation rights attached to it.

Transfer Disclosure Statement (TDS) – CC §1102

The TDS is the foundation of California buyer disclosures under contract. It covers the seller’s known material defects across roof, plumbing, electrical, structure, pest, HOA, legal claims, and deaths within the past three years. Sellers are required to complete it even in as-is sales.

Under CC §1102.13, a seller is liable for actual damages resulting from non-disclosure.

Four things to check in every TDS:

- Every “Yes” answer. Each one requires documentation, not just a written description. Ask for it.

- Repaired issues. The seller still must disclose them. For anything listed as repaired, request the contractor invoices.

- Prior inspection reports. Any report in the seller’s possession must be shared with you, even if it is stamped “non-transferable.”

- Blank fields. These are not acceptable. Request completion before you remove any contingencies.

Seller Property Questionnaire (SPQ) – C.A.R. Form SPQ Rev. 12/24

The SPQ supplements the TDS with the history of repairs, permits, fill and grading, prior inspections, insurance claims, and drug lab disclosures. Two new disclosures were added in 2025: an electrical inspection advisory under CC §1102.6i and a gas appliance replacement requirement under CC §1102.6j.

When reviewing the SPQ, focus on prior inspection reports the seller has commissioned, any unpermitted additions or structural changes, and prior water, fire, or mold insurance claims, even if the seller describes them as resolved.

Natural Hazard Disclosure (NHD) – CC §1103

California is the only state that mandates this specific form. The NHD covers six mandatory hazard zones: flood, dam inundation, Very High Fire Hazard Severity Zone (HFHSZ), wildland fire, earthquake fault, and seismic hazard.

If the HFHSZ box is checked, verify insurer availability before you remove your contingencies. Many California carriers no longer write new policies in these zones.

If the CA FAIR Plan is your only option, understand what it covers:

- Fire, yes.

- Earthquake, flood, and liability, no.

For Mello-Roos and special assessments, get the exact dollar figure from the title company rather than relying on the NHD estimate.

For earthquake fault zones, standard homeowner’s insurance excludes seismic events. Get a California Earthquake Authority quote before you commit.

Agent Visual Inspection Disclosure (AVID) – CC §2079

The AVID is the listing agent’s independent visual inspection of the property. It must be delivered within 7 days of acceptance and completed before contingency removal. Any divergence between what the AVID documents and what the TDS states is a red flag that requires immediate follow-up. Late delivery of the AVID is a compliance issue worth flagging with your agent.

California-Specific Certifications

- Water heater seismic strap certification (CA H&S §19211). The seller certifies the water heater is strapped per California law. Verify this physically during your inspection. A missing strap is a code violation, not a maintenance recommendation.

- Smoke and CO detector compliance (CA H&S §13113.8). Operable smoke detectors are required at time of sale. CO detectors are required for homes with attached garages or fossil fuel appliances.

- Lead-based paint disclosure (pre-1978 homes). You receive a 10-day testing window that is technically waivable. Do not waive it if you are planning any renovations.

- Fire Hardening Disclosure (FHDS). Required for properties in HFHSZ under CC §1102.6f.

- HOA documents (CC §4525). If the property is part of an HOA, you receive CC&Rs, bylaws, the current budget, reserve study, recent meeting minutes, pending litigation disclosures, and master insurance information. A reserve fund below 70% is a reliable signal of future special assessment risk.

One right most buyers do not know about:

A supplemental disclosure restarts your cancellation clock. If the seller amends the TDS at any point – even after you have removed all contingencies – you have 3 days (personal delivery) or 5 days (electronic delivery) to cancel under CC §1102.3(c). This right expires automatically. You do not need a formal contingency waiver for it to apply.

Stage 4: Closing – Closing Disclosure and Loan Documents

Reviewing California Buyer Disclosures at the Finish Line

Two documents define the closing stage. Both require careful review before you sign anything.

Closing Disclosure

The Closing Disclosure is the final document in the TRID sequence, and it arrives at least 3 business days before you sign loan documents. That window exists for a reason: use it.

This is your last opportunity to catch lender fee increases. Compare it line-by-line against your Loan Estimate using these tolerances:

- Section A (origination charges): Cannot increase at all. Any increase is a TRID violation.

- Section B (lender-required services): Cannot increase by more than 10% in aggregate.

- Section C (services you can shop): No tolerance limit if you chose a provider not on the lender’s list.

- Prepaid items (taxes, insurance, interest): These can change based on your actual closing date.

If you find an error or an unexplained increase, contact your lender immediately. Lenders can issue a corrected Closing Disclosure, which resets the 3-day review window. That is not a delay – that is you exercising a right that exists specifically for this situation.

Promissory Note and Deed of Trust

These are the documents you sign at the closing table. The promissory note is your legal promise to repay the loan. The deed of trust gives the lender a security interest in the property, which is the legal basis for foreclosure if you stop making payments.

- Before you sign either document, confirm that the interest rate, loan amount, monthly payment, and prepayment penalty terms match the Closing Disclosure exactly.

- If anything differs from what you expected, stop and ask. Do not sign until the discrepancy is resolved.

How ficustree Supports Every Stage of California Buyer Disclosures

Most tools help with one part of the process. ficustree is built around the full California buyer disclosures journey – from the first BRBC question through the Closing Disclosure comparison at the end.

| What buyers do today | What ficustree does | Buyer outcome |

|---|---|---|

| Sign the BRBC without reading the exclusivity clause or understanding commission exposure | Surfaces the BRBC’s key terms before signing: exclusivity status, compensation amount, and what happens if the seller does not pay | Buyer enters the agency relationship with clear eyes, not surprises at closing |

| Apply to one lender and accept the first Loan Estimate without comparing | Prompts buyer to compare Loan Estimates across lenders; highlights Section A origination charges where lenders vary most | Typical savings: $2,000 to $5,000 in origination fees from same-day comparison |

| Receive a 60-page disclosure packet and sign acknowledgment without fully understanding it | Parses TDS, SPQ, NHD, and AVID simultaneously – classifies every flag by severity, surfaces cross-document conflicts | Clear priority list within minutes, not hours of reading |

| Miss California-specific issues: HFHSZ, seismic strap, Mello-Roos, FPE panels, knob-and-tube wiring | Purpose-built California detection engine – flags items other tools miss entirely | No California-specific blind spots at any stage |

| Realize the Closing Disclosure has higher fees than the Loan Estimate – too late to act | Compares Closing Disclosure to stored Loan Estimate automatically; flags any out-of-tolerance fee increases | Catches lender overages before the 3-day window closes |

| Confused about which deadlines apply when – misses a cancellation window | Tracks delivery timestamps for every document across all 4 stages; alerts buyer to active cancellation or review windows | Never miss a legal right because of a missed deadline |

Frequently Asked Questions About California Buyer Disclosures

What documents do California home buyers have to sign?

California buyer disclosures span four stages. Before your first tour: the BRBC and Agency Relationship Disclosure. During mortgage application: the Loan Estimate and Intent to Proceed. Under contract: the RPA, TDS, SPQ, NHD, AVID, lead-based paint disclosure, seismic strap certification, and smoke/CO detector compliance (plus HOA documents if applicable). At closing: the Closing Disclosure, promissory note, and deed of trust. That is 14 or more legally significant documents in a standard transaction.

Do I have to sign the BRBC to attend open houses?

No. Open houses you attend on your own, without an agent, are generally exempt from the BRBC requirement. The requirement applies when a buyer’s agent accompanies you or is involved in showing you a property. As soon as you engage an agent for an MLS-listed showing, the BRBC applies before that showing happens.

What if the seller’s agent refuses to pay my buyer’s agent commission?

Under the post-NAR settlement model, this is now possible. Your BRBC specifies who is responsible if the seller does not cover the fee. In many transactions, buyers ask sellers to include a concession toward the buyer’s agent fee as part of the offer. If the seller refuses and your BRBC holds you responsible, you owe your agent the agreed amount. This is exactly why understanding your BRBC terms before signing matters.

When do I get the Loan Estimate after applying?

Within 3 business days of submitting a complete application. A complete application requires your name, income, Social Security number, property address, estimated property value, and loan amount. Before all six pieces of information are submitted, the lender has no obligation to issue a Loan Estimate, regardless of any preliminary conversations you have had.

Can I switch lenders after signing the Intent to Proceed?

Yes, but there are real costs. Your appraisal fee (typically $500 to $1,000) is lender-specific and usually non-refundable. Any rate lock fee is also typically forfeited. Switching lenders mid-transaction also delays closing, which can trigger a Notice to Perform from the seller. Do your lender comparison before you sign the Intent to Proceed.

Can I cancel the contract based on disclosures after contingencies are removed?

Only if a new or amended disclosure arrives after removal. Under CC §1102.3(c), an amended TDS or SPQ revives your right to cancel: 3 days after personal delivery or 5 days after electronic delivery. Once that window closes, it expires automatically. No other previously waived contingency is revived alongside it.

What fees can the lender raise between the Loan Estimate and Closing Disclosure?

Under TRID, Section A origination charges cannot increase at all. Section B and C third-party services can increase by no more than 10% in aggregate if you used the lender’s recommended providers. Prepaid items such as per-diem interest, taxes, and insurance can change based on your actual closing date. Your cash to close may also change if your down payment or loan amount changed.

Sources and Legal Citations

All legal citations are current as of April 2026.

| Ref | Data point | Source |

|---|---|---|

| [A] | BRBC required before first MLS-listed tour (NAR settlement); by no later than offer per AB 2992 (effective Jan 1, 2025); max 90-day term, void if exceeded | CA DRE Licensee Advisory Nov 14, 2024 ; Tyler Law LLP “New C.A.R. Forms for 2026” Nov 2025 |

| [A2] | BRBC defaults to non-exclusive; exclusive requires separate initialing of para 15; cancellation 30 days notice if exclusive | RHRC.net “Introduction to BRBC” (2024) ; BRBC draft / sample form (public PDF) |

| [B] | Loan Estimate required within 3 business days of complete application | CFPB TRID FAQ ; Rocket Mortgage (TRID guide) |

| [B2] | No fees before Intent to Proceed except credit report; Closing Disclosure 3 business days before signing | CFPB Closing Disclosure explainer ; Bankrate Closing Disclosure guide |

| [C] | TDS required CC §1102; 3-day/5-day cancellation rights; supplemental disclosure revives cancellation rights CC §1102.3(c) | CA Civil Code §1102–§1102.14 ; BPE Law (2021) ; C.A.R. RPA public sample (7/24 PDF) |

| [C2] | SPQ Rev. Dec 2024; new 2025 disclosures CC §1102.6i (electrical) and CC §1102.6j (gas appliance) | Tyler Law LLP “New C.A.R. Forms for 2026” ; C.A.R. Form SPQ Rev. 12/24 (public PDF) |

| [C3] | NHD required CC §1103; 6 mandatory zones | CA Civil Code §1103.2 ; SnapNHD ; FastNHD |

| [C4] | AVID required CC §2079; delivered within 7 days; completed before contingency removal | Rise Realty CA (2026) ; C.A.R. Form AVID public sample (6/24 PDF) |

| [C5] | Lead paint disclosure 42 USC §4852d; water heater seismic strap CA H&S §19211; HOA docs CC §4525 | Federal HUD/EPA lead disclosure guidance ; 42 USC §4852d ; CA H&S §19211 ; CA Civil Code §4525 |

| [C6] | Sellers must disclose all prior inspection reports in their possession, even if "non-transferable" | Rise Realty CA “AVID 101” Jan 2026 ; C.A.R. AVID public sample / reference |

Disclaimer

Educational purposes only, please conduct your own due diligence

This article covers four stages of the California Buyer Disclosures + homebuying process and is intended for general educational purposes only. It is not legal, financial, or mortgage advice. California real estate law, federal mortgage disclosure requirements, and C.A.R. form versions change regularly. The information in this guide reflects statutes and forms current as of April 2026.

BRBC: The Buyer-Broker Representation Agreement is a legally binding contract. Have it reviewed carefully before signing. Agent compensation structures vary by transaction. Consult a California real estate attorney if you have questions about your specific agreement.

Loan Estimate / TRID: Fee comparison guidance is general. Actual fees vary by lender, loan type, property, and transaction. Consult a licensed mortgage professional for advice specific to your loan.

Seller disclosures: Consult a licensed California real estate agent and real estate attorney before removing any contingency or making decisions based on disclosure documents.